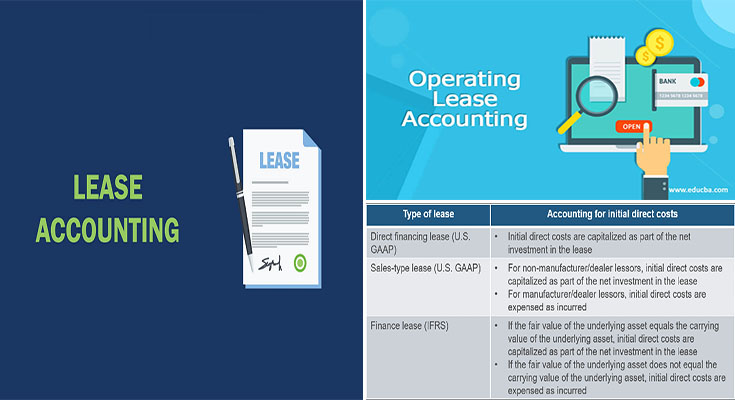

Capital vs. Operating Lease: Finance Lease Accounting Rules

The distinction between capital and operating leases is a fundamental concept in lease accounting that impacts how leases are treated on financial statements. Understanding the rules for finance lease accounting can provide clarity on how these leases are recognized, measured, and disclosed in financial reporting. In this article, we will explore the finance lease accounting rules for capital versus operating leases.

Capital Lease Accounting

A capital lease is a type of lease that effectively transfers the risks and rewards of ownership from the lessor to the lessee. Under lease accounting rules, a capital lease is treated as a purchase of the leased asset, and both the asset and liability related to the lease are recorded on the lessee’s balance sheet.

- Recognition: The lessee recognizes the leased asset and the corresponding lease liability on the balance sheet at the present value of the lease payments.

- Amortization: The lease liability

finance lease and operating lease Securities are companies or parties that obtain financing in the form of capital goods from the lessor. Lessee in economic lease aims to get financing in the form of goods or equipment by way of installment payments or periodically. At the end of the contract, the lessee has option rights over the item. That is, the lessee has the right to buy goods leased at prices based on residual values. In an operating lease, the lessee can fulfill the needs of his equipment in addition to the operator and maintenance of the tool without risking the lessee to damage.

finance lease and operating lease Securities are companies or parties that obtain financing in the form of capital goods from the lessor. Lessee in economic lease aims to get financing in the form of goods or equipment by way of installment payments or periodically. At the end of the contract, the lessee has option rights over the item. That is, the lessee has the right to buy goods leased at prices based on residual values. In an operating lease, the lessee can fulfill the needs of his equipment in addition to the operator and maintenance of the tool without risking the lessee to damage.